Some heavy topics are afoot at tomorrow’s school board meeting and I have addressed a couple of them in my recent posts. But one recurring issue needs more attention and it goes to the question of the district’s current financial operating performance.

If the district is continuing to add to fund equity, how does that affect our views on employee compensation and policy changes aimed to increase enrollment?

The very fact that the Board will even entertain the policy change to allow non-resident staff to enroll their children in GPPSS schools is evidence enough that there is concern about revenue. Paint or spin however you wish, but the only reason to enact such a policy is to increase revenue.

Meanwhile some district spokespeople have avoided discussion of employee compensation on the basis that fund equity continues to increase. This position is hard to reconcile with a decision to enact the above mentioned policy change, which is why the discussion tomorrow should be so interesting. But leaving that aside, let’s look at the operating budget.

Fund Equity increases when the district runs an operating surplus. The goal since 2010 has been to achieve a 10% fund equity (as a percentage of expenditures). From a high of 20% to a low of 2%, this has been a rocky ride that appears to be stabilizing around 8%. The issue is whether there is momentum not only to achieve the 10% goal, but also to enable the replenishment of operating budget sources for areas that were slashed in the late 2000’s. Technology spending is the best example. Other would fairly argue for restoring salary compensation.

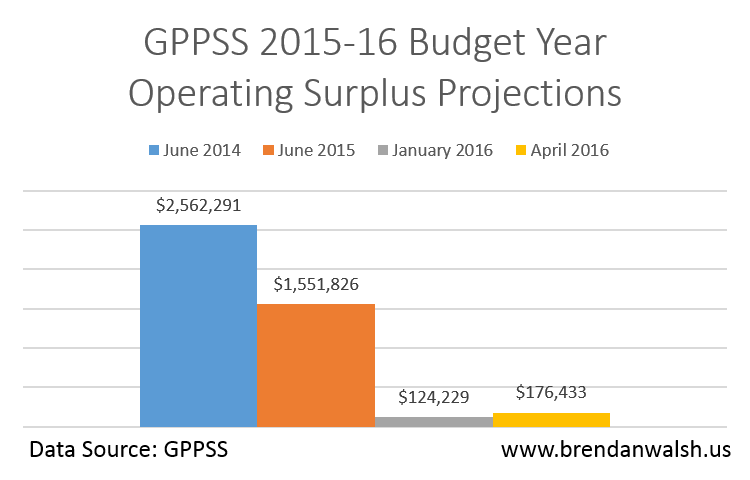

Examining the annual operating surplus is critical to all this and the district makes these projections fairly frequently – typically when they adopt or amend the budget, which it just so happens the Board is voting on tomorrow. So I went back and looked at the last four iterations of the 2015-16 (current year) operating surplus and this is what the projections have been.

The brief interpretation here is that projections have become, generally, increasing less optimistic from June 2014 until now. But with district data, we can isolate what the big moving pieces are.

Let’s focus on the delta between the most recent (April 2016) projection and the June 2015 one, which was the adopted budget. The biggest delta is revenue. (For wonks, I am leaving out state MPSERS UAAL revenue which is a pass-through.) Revenue projections are down $1.8 million from a year ago. This is most likely attributable to lower than expected enrollment and lower than expected county aid.

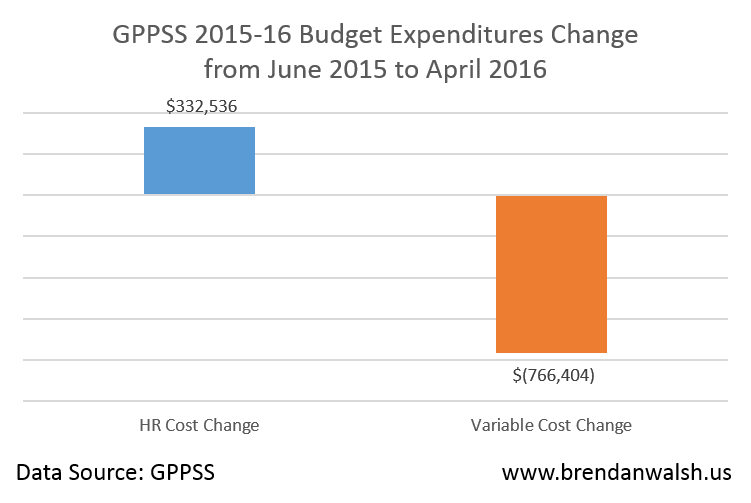

With $1.8 million less revenue we would expect the drop projected surplus – and perhaps even an operating deficit. If even now the district projects a $176,433 operating surplus given $1.5 million lower revenue, this means expenses would have to be reduced by $434,000. To keep things really simple we can break expenses down into two categories – human resources costs and other variable costs. Here’s the total changes in these categories from the originally adopted budget until now.

We could keep crawling into this spider hole, but the big picture point should be clear. It is a dangerous and ultimately counter-productive strategy to rely upon continually cutting non-human resources expenses to accommodate rising human resources expenses (and a healthy dash of declining enrollment).

One that really jumps off the page is textbook investment. The district traditionally budgeted $400-$500,000 for textbooks annually. This year they budgeted a mere $50,000. That’s not a sustainable or structural budget solution.

Another worth noting is Repairs and Maintenance. We hear frequently in the bond forums the need to invest more here, but this year the budget is $1.2 million – which is actually an increase over last year, but far short of the $2 million that it averaged from 2007 through 2012.

These are some of the dynamics and trends the Board, Administration and community need to reconcile as we take on structural policy and budget change.

One response to “Structural change or fingers in the dike?”

[…] annual loss of $635,000 is $2.2 million worse than the district’s original budget plans that had forecasted a $1.5 million surplus and $455,000 worse than its last budget amendment. The […]